|

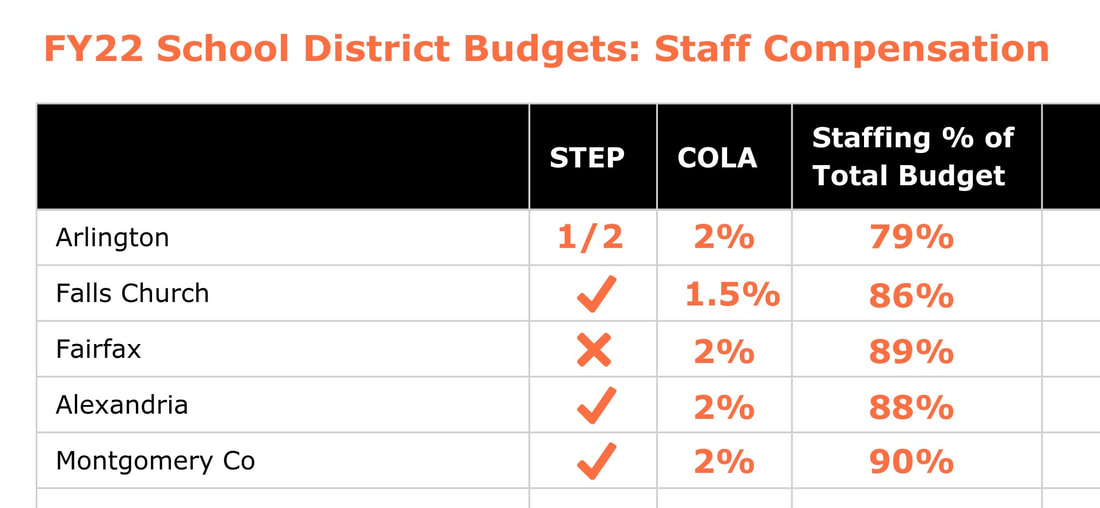

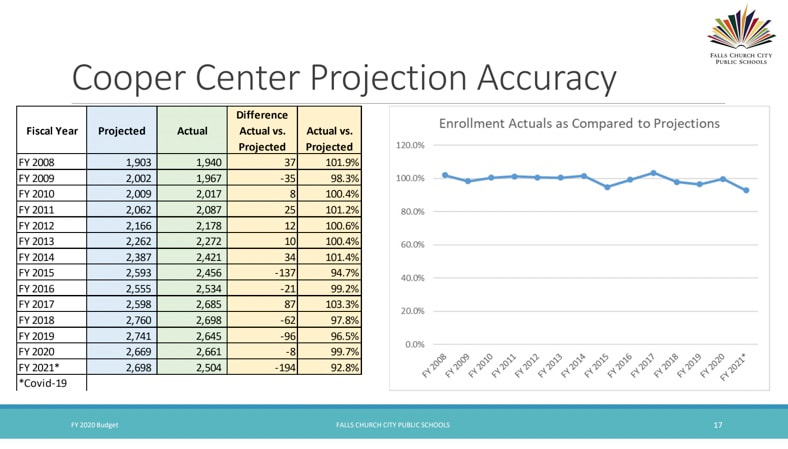

Early in my School Board campaign I received some great advice: a recommendation to read closely the end-of-year reports of the various APS citizen advisory committees. Community volunteers contribute considerable expertise and literally thousands of hours of work each year to collaborate with APS leaders and the School Board, and their informed perspectives are worth studying. As I continue to listen and learn over the summer I’m going through these end-of-year reports, starting with the recently published work of the Budget Advisory Council. I’ll be using these campaign emails to share highlights with you, along with my own questions and ideas. Why start with the budget, and why talk about it now? Earlier in the campaign I flagged the concern that APS is projecting a shortfall of more than $100 million by 2025. I think this merits a sustained and collaborative effort to ensure that our school system is on stable financial footing. Below are some of my reactions to the Budget Advisory Council’s end-of-year report, adding in my own study of the APS budget and investigation of how other local school districts develop their budgets. There's a lot to consider in the BAC's report, so I'm going to be emailing key takeaways in two parts--here's Part One. 1. We should talk about “zero-based” versus “baseline” budgeting. APS prepares its budgets through a method called “baseline budgeting” in which the prior year’s adopted budget is the starting point for building the next year’s budget. The previous budget gets reviewed and modified to reflect any necessary increases or decreases, and the resulting new budget line items are usually presented as a percent change up or down from the previous year. There are many advantages to baseline budgeting, not the least of which is the ability to easily track increases and decreases from previous years. However, it’s all too easy to carry forward items year to year without careful review and justification of expenses. For that reason, many school districts including those in Loudoun, Alexandria and Montgomery County use “zero-based” budgeting instead. LCPS describes its budget as “built based on actual needs without particular regard to previous funding.” ACPS notes that this requires staff to “scrutinize each line item and build their budgets from the ground up.” Given our projected shortfalls, building from the ground up—without assuming business as usual—sounds like it has merit. If APS can’t utilize zero-based budgeting, I believe it should consider more regular, formal evaluations of return on investment as other school districts are doing (what I described as “academic ROI” in my campaign platform.) 2. We should talk about “needs-based” versus “balanced” budgeting. One of the few differences of opinion I have with the BAC is its recommendation that the Superintendent present a balanced budget versus a needs-based budget, which has been the practice over the past few years. Without a doubt, it would be less painful for all involved if the Superintendent presented a budget that’s already balanced, but I think it’s the wrong move for two reasons. First, the Code of Virginia requires district leaders to develop needs-based budgets that reflect the total funding needed to operate schools. As ACPS notes, “It is then the responsibility of the School Board to balance the needs of the school division with the considerations of the economic and political environment.” The second reason to present a needs-based budget is that the community needs to understand the actual costs of operating its schools—and it deserves a voice as the School Board makes the hard choices that may be required to balance the budget. 3. We need to build in the full cost of staffing. Our budget reflects our values. If we believe that our staff is our greatest asset (and indeed, research confirms that there is no greater school-based influence on student achievement than access to a qualified, caring teacher), then our budget should reflect that by fully funding staff salaries. It’s wonderful that in its FY22 approved budget the School Board was able to fund a 2% increase for all staff and a STEP increase midway through the year. (If you don’t understand what a STEP is, see here.) Still, it troubles me that the School Board’s Budget Direction to APS leadership last fall included a waiver of its own policy that requires the Superintendent to include the STEP increase in each year’s proposed budget. (And this is not the first time this policy has been waived.) Why aren’t we building the full cost of staffing into our needs-based budget? Fully funding the STEP increase costs APS $10.6 million. Each 1% cost of living adjustment (COLA) costs $4.6 million. APS’s total approved FY22 budget is $700 million. I’m also curious why we aren’t able to fully fund the STEP increase when several other local school districts are doing so. Examples:  4. We need focused effort on, and transparent accounting of, enrollment projections. As the BAC noted in its report, enrollment projections are fundamental to building the budget. APS is continually working to improve the process by which it forecasts enrollment; it would be helpful, I think, for the School Board and the community to have a clear sense of whether those efforts are bearing fruit. When I looked at the Falls Church City Public Schools FY22 budget, I was struck by information that FCCPS included on the accuracy of its enrollment projections:  Given how important these projections are to our budgeting, I’d love to see similar reporting included in our APS budget. (I believe I’ve seen something like this from APS before, but it’snot in the current budget and I wasn’t able to find it on the APS website.) If our projections are not as accurate as we’d like and/or not improving over time, perhaps we could explore working with different outside consultants to generate the projections.

5. We need to look for cost savings in transportation, energy use, class scheduling, and more. Here I quote the BAC (and paraphrase what APS itself suggests in the FY22 budget): “With a projected deficit of over $100M by FY25, we need to start planning more than one budget year at a time, and we need to identify structural rather than one-time cuts that reappear in the following year’s budget. We should do serious studies on every one of the long-term budget savings ideas that show up in the Long-Term Savings Section of the FY22 Proposed Budget Executive Summary to determine whether there are real savings to be captured.” I wrote about Transportation in May and want to keep listening and learning to understand how we can become more cost-efficient and environmentally friendly. I’m also keenly interested in how APS energy savings might dovetail with Arlington County’s goal to become a carbon-neutral community by 2050. I also continue to believe that there are cost savings we can achieve by improving our class scheduling within existing class size limits. I wrote about this in March and in a January letter to APS, which also suggested that APS explore the idea of employing class size averages instead of a ceiling. (Some have used this to argue that I am in favor of increasing class size—which is not my position. I am trying to find creative solutions that don’t yield larger classes across the board.) Studies suggest that districts who increase their scheduling efficiency and/or adopt class size averages are saving tens of millions of dollars. In my next email, I’ll talk about a few steps we could explore to improve the budget process and format, plus one idea to increase revenue (no tax increases involved). Comments are closed.

|

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

October 2021

Categories

All

|

RSS Feed

RSS Feed